Corporate Credit Keeps Partying While Bears Ponder How To Crash It. Meanwhile Stocks...

Corporate Credit Keeps Partying While Bears Ponder How To Crash It. Meanwhile Stocks...

Credit in its own world; CRE in its own hell; "What about the yield curve and private credit?" you say; And stocks are still all about buybacks.

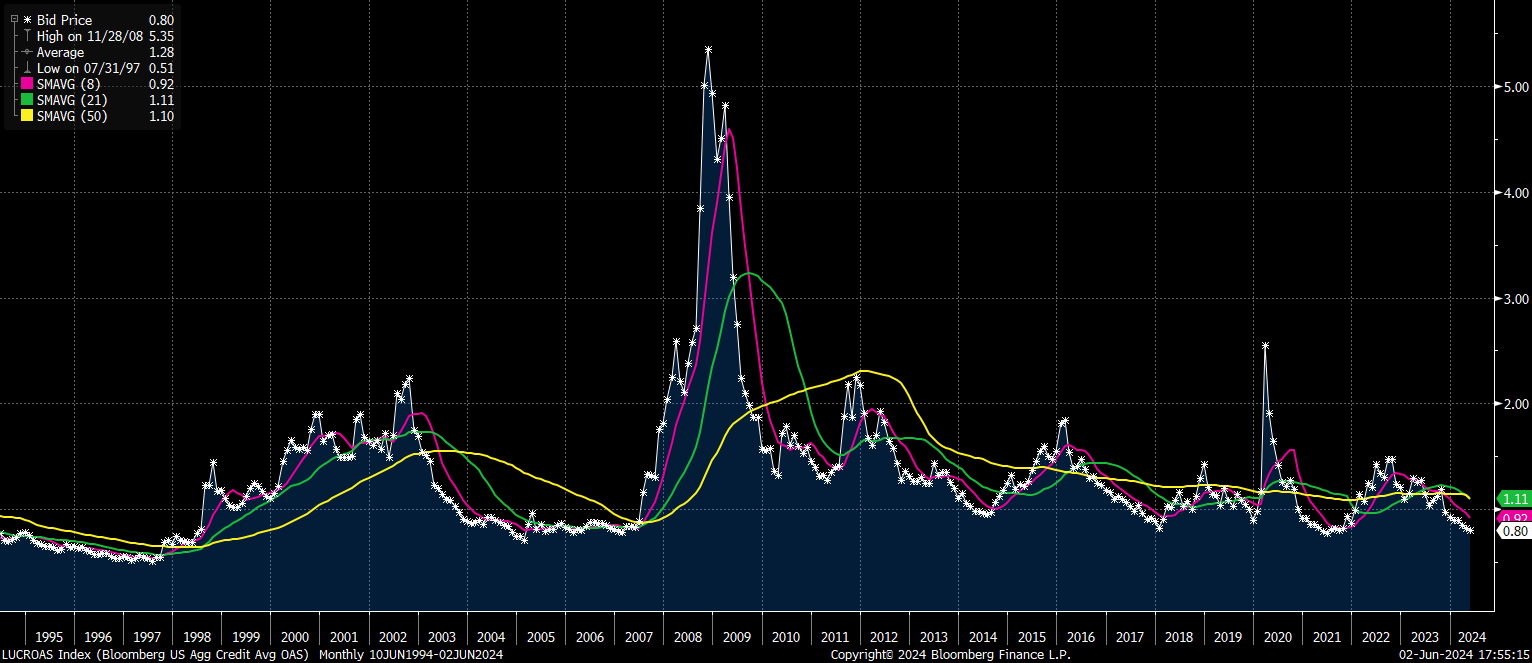

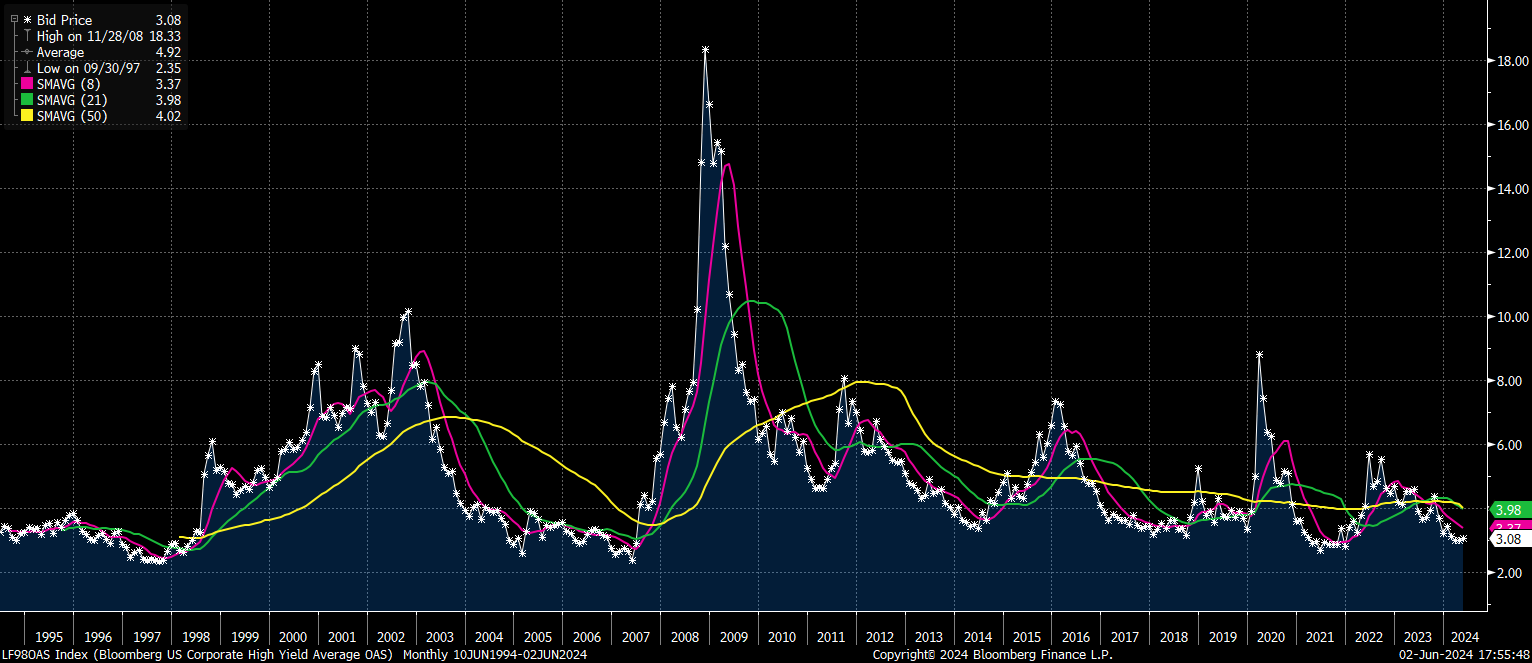

I will start with the good - and by far most important - part of the program. Corporate credit remains on fire. YTD corporate issuance has already crossed the $1T mark, and it’s on pace for the first $2T year aside from the Covid/Fed influenced 2020 and 2021. So, in case you are in the camp that higher Treasury rates will crush large companies’ balance sheets, it may be time to reconsider. And if the mere volume of issuance were not enough, both Investment Grade and High Yield risk spreads are scraping the tightest levels in decades.

It can’t be repeated enough that bond issuance is the lifeblood of buybacks and M&A, and for decades buybacks and M&A have provided the only net buying of stocks to the tune of almost $7 trillion dollars. And the beat goes on. Companies continue to up their repurchases with $588B of new announcements YTD, more than 80% of the annual average between 2017-’23. Air pockets in stocks - or even deep corrections - notwithstanding, it will be nearly impossible for bears to kill this equity bull market without credit caving ahead of it.

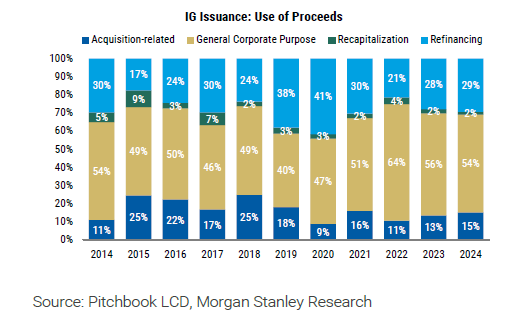

A couple of related issues raised by some of my Twitter followers. First, is the question of whether the gargantuan YTD issuance is simply to refinance existing bonds and not earmarked for buybacks and/or dividends. As you can see in the chart below, that’s really not the case. The use of proceeds from new issuance remains very much in line with historical levels.

Second is the evergreen fear stemming from the long tail of PTSD from the Great Financial Crisis: weren’t risk spreads also uber-tight right before the GFC? Yes they were, but the structural backdrop for corporate credit could not be more different now than the middle of 2007. That’s when the credit crisis began in earnest, led by early signs of stress in the Municipal Auction Rate Securities, which back then was one of the deepest and most liquid markets. The MARS market would ultimately collapse in late January ‘08, but stocks hardly noticed until May of ‘08.

There are many measures of credit-markets health, but here is a quick recap from Morgan Stanley’s mid-year outlook which came out at the end of last week:

“For IG companies, cash-to-debt ratios remain very healthy compared to history. While lower than the 2021 peak, cash levels remain well above the long-term median. While gross leverage has been sideways for a few quarters, net leverage has actually declined over the same period. Interest coverage for IG companies also remains significantly above the long-term median. While coverage will likely weaken over time as more debt rolls into current coupons, this will be a long, drawn-out process that takes years, not quarters… As a by-product of balance sheet resilience, the IG corporate market has seen quality actually improve in the last two years. Upgrades have outpaced downgrades and single-As now account for a bigger part of the index today than three years ago (at the expense of BBBs). Note that this was all backward-looking resilience when earnings growth was very sluggish. Consensus expectations point to EBITDA growth of 24% by 4Q24 for IG companies.”

Again, compare this narrative to a time when a large institutional market of short-term municipal obligations froze almost over night.

So what could cause corporate credit to eventually cave in? The most obvious area of trouble remains Commercial Real Estate. Yes, almost everyone with a pulse is already aware of the CRE problems, but I don’t get the sense that generalists realize how dire things are. A few months ago I wrote “the credit problems stemming from the “cyclical (secular?) winter” engulfing commercial real estate - primarily office, but residential may be the next shoe in 2-3 years - are nowhere close to the end; in fact New York Community Bank (NYCB) may be the first salvo. We will see if banks can bring us a sequel to the 2010-2012 “extend and pretend” thriller, and smooth out the pain without shocking the system;…”.

Since then the landscape has only worsened. As a mortgage broker with a very large multinational firm put it to me, residential projects that came out of the ground pre-Covid and are slated to refi out of contruction loans and into permanent financings are known as “foreclosures”. Meanwhile, forced sales of offices in the class B+ or lower tier are going for the value of the land minus demolition costs. If 6-12 months ago “extend and pretend” was tantamount to pulling a rabbit out of the hat, that rabbit has grown into the size of kangaroo. Healthcare REITs are in shambles, and even the safe haven of Storage facilities is weakening.

I know there are hundreds of billions of dollars rotting in the bank accounts of distressed credit funds, so at some price there will be bids, and those bids will likely prevent a systemic accident, but the potential for ugly damage to the credit markets remains.

A more arcane risk remains the 2s10s yield curve. I have been on record for more than a year saying that the inversion which began more than two years ago showed many signs of being different than the inversions that preceded the ‘00-’02 and ‘07-’09 credit collapses, and by now there’s no arguing that the course of this inversion has been different. The gazillion dollars question is whether what will happen once the curve re-steepens will also be different. If the answer is no, then the last two meltdowns will seem like a walk in the park. But front-running a credit collapse has always been a suicide mission, and this time it has the added uknown of whether the outcome of the re-steepening will also be different.

Next there is the issue of private credit. Since the end of the GFC, when traditional banks were neutered into being the financial equivalent of electric utilities, private credit has taken over most of the credit foodchain, from re-discount lending to private label subprime credit card issuers, to plain-vanilla direct loans to small and mid-market enterprises, and everything inbetween. The 10+ years post GFC has been the golden age of private finance, but now this asset class is front page news, a lot of money is chasing it, and the quality of the deals is inevitably dropping. These assets are as illiquid as they come, and when deals go sideways there’s no way out of them. Just last week a small Canadian funds family suspended distributions. By itself this is a non-issue, but there’s lots of institutional money (read pension and insurance funds) counting on those distributions to meet their liabilities. Large scale failures are not an option, and systemic risk is absolutely there. Again, I am highlighting this as a potential risk, not an imminent risk.

And lastly the biggest risk to credit remains always the same one: something coming out of left field for which no one is prepared. Good luck preparing for that.

So where does that leave stocks? There are far smarter people than me suggesting where stocks are going to go next, and besides, in my humble opinion it is impossible to express an outlook for equities without attaching a timeframe to it. To my eyes, and through the lenses of DeMark technical indicators, stocks in the short-to-intermediate term (over the next 6 months or so) are heading toward a series of rolling upside exhaustion signals. QQQ 0.00%↑ $466 and SPY 0.00%↑ $543 look like tough hurdles for a while. But longer term (on monthly charts) both DeMark indicators and traditional technical patterns still look healthy, and - consolidations/pullbacks notwithstanding - that’s not likely to change as long as corporate credit stays strong.

I know this next sentence will be villified by bears and contrarians, but broad market valuations have not mattered for a long time, and continue not to matter. Uber expensive sectors (I am looking at you software stocks IGV 0.00%↑) have been crushed of late in favor of anything Semis SOXX 0.00%↑, “AI”, and many industrials. This is entirely consistent with the notion that cyclical/rolling bear markets in different sectors is what allows broad indices/secular bull markets to continue to levitate, as proceeds from buybacks get reinvested in passive…ish baskets.

So watch credit, pick your time frames, and don’t be a hero on the short-side: as long as credit holds, buybacks WILL continue for longer - and get bigger - than any short can remain solvent.

Good luck!